As is so often the case, it is difficult to find in the ongoing daily flow of news why the US dollar is presently so weak, plumbing its historic record lows.

Based on monetary theory, the value of a currency is the inverse of the inflation of the currency (inflation refers to the increase in the supply of money relative to goods and services produced, or in simple terms, the progressive loss of value of a currency).

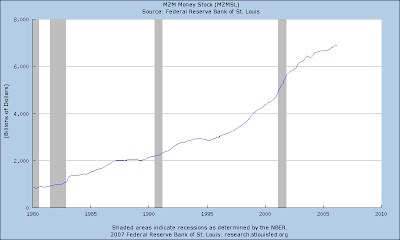

However, the US is about "equally bad" to most of the world's other major economic powers with respect to increasing the quantity of its money.

France, for example, is horrible, and has recently separated itself from the other nations sharing the Euro by announcing plans to spend its way to prosperity.

Those with old-fashioned values will recognize that historically, both individuals and nations have been more likely to attain prosperity by saving rather than spending, so it is difficult to see how France’s “new plan” will engender anything other than soaring government debt, inflation and currency devaluation.

China, in addition to announcing record foreign reserves (mostly in US dollars) of $1.33 trillion, has also acknowledged that its current money supply growth continues to run at a bubble-inducing clip of 17.06%, almost double the approximate (and still profligate) 10% rate of money supply growth in the United States. (The Chinese rate of money supply growth has topped 20% in the recent past, though also note that the portion of this growth that is counterbalanced by increased production of goods and services is not inflation-inducing.)

So, why is the US dollar so weak?

It has often been remarked that financial markets are a discounting mechanism for the future. Therefore, the weakness in the US dollar is not a reflection so much of the present deplorable state of US monetary inflation as it is of anticipated continued weakness to come.

After all, the US is probably no worse than most of its peers in a global environment where virtually every major power is attempting to “spend its way out of debt” to avert looming economic weakness.

No, the problem with the US dollar is that the prospects for the US economy for many years to come appear inferior to those of its peers. This in itself would not be sufficient to weaken the US currency. But the financial markets are also betting that the US will respond to future economic difficulties by continuing to spend, spend and spend – and that this irresponsible policy will be supported by incessant, virtually neverending inflation of the US money supply.

Why, then, is the US situation so much worse than that of the other major powers?

It is not difficult to figure this out.

(1) The United States is attempting to maintain its status as the world’s primary super power through massive expenditures for non-productive military equipment and adventures. The Bush government is attempting to preserve America’s security and pre-eminence through military interventions which counter-productively increase the number of its adversaries on a daily basis, thereby requiring continued escalation in military expenditures as far as the eye can see.

(2) The United States maintains the world’s worst current account deficit, driven primarily by an appalling trade deficit, approaching $1 trillion per year. Even when American revenues are falling, Americans can't stop spending, and so they are running up an international “credit” bill that is unparalleled in world history.

(3) Speaking of American spending, no one in the world is so deeply indebted as the average American consumer. American mortgage debt accumulation of the past 6 years equals the combined mortgage debt accumulation of the previous half century (50 years). Americans maintain record levels of consumer debt, and have precipitously declining levels of equity in their homes, which are now also declining in value – and will be doing so for many years to come.

(4) American governments cannot say no to the demands of competing interest groups, with the result that virtually every interest group gets paid off, with a particular premium being afforded for the US military, as already discussed. As is also true of Canadians, Japanese and Europeans, Americans are aging at a rapid clip, so there will be more retirees depending upon more government entitlements for health and social security outlays. This problem is multiplied by the failure of American corporate retirement plans due to already-occurring or looming bankruptcies in such sectors as airlines and manufacturing (think Ford and GM) which force the government into the lurch to cover these costs as well. Massive though this problem already sounds, consider also that Americans have not yet set aside the social security and health insurance funds needed to cover these costs. These funds will be drawn from future (and possibly declining) government tax revenues, which will force either tax increases or – think about it – continued devaluation of the currency to make it possible for government to continue allocating these massive payments.

(5) Countries such as Canada and Germany – as well as the emerging Asian powers – export more than they import, providing a source of national income to meet future expenditures. This places the United States, the world’s record debtor, at a massive relative disadvantage to the nations of the world which have a stronger productive base due to marketable exports.

The US dollar is therefore declining because financial markets are actively anticipating that the United States will fail to resolve such problems as the five noted above. This failure will force the US to continue devaluing its currency for decades to come, and global investors are presently speculating that the United States will have more difficulty meeting its financial commitments than will the majority of the world’s remaining major economic powers.

In other words, the US dollar is in relative decline today not because the US is presently inflating its currency more than other nations, but because in future, the US will be forced to inflate while its peers will be able to retrench by raising interest rates and curbing money supply growth relative to the United States.

This pattern is already visible, with interest rate rises just announced in Canada and the Euro region, while Mr. Bernanke in the US sits on his hands, hoping to maintain the flow of easy money to resolve his nation’s far more serious underlying fiscal problems.

It is no secret that Mr. Bernanke (Chairman of the US Federal Reserve Board, or FRB) is caught between a rock and a hard place. If he raises rates to match his global peers, he risks launching the United States into a major recession, which in turn would almost certainly derail the international economy. If Mr. Bernanke lowers rates, this will maintain the flow of liquidity, but at some point, this policy would fuel inflation to levels that could not be disguised, correspondingly lower the value of US assets, and risk launching the US dollar to record historic lows.

If you were Mr. Bernanke, what would you do?

At present, Mr. Bernanke continues to do nothing, neither raising nor lowering US interest rates. So far, his bluff has not failed. The problem is that when he takes action – whichever action he takes – a crisis will be difficult to avert.

And from a long-term view, this is inescapably bad news for the US dollar.

ADDENDUM (15 July 2007): There can be no doubt that the US dollar is due for a technical bounce to the upside, based on being severely oversold at present. However, the dollar's recent action breaks its previous pattern by being unusually weak.

For some time, we have been waiting for a real test of the .78-.80 level on the US Dollar Index. We may now be there. Clive Maund, a wise, respected and objective technical analyst, has just published a paper entitled "Dollar at the Rubicon."

Should the US dollar now fall below the .78 figure following an upside bounce, say by late July or August, this could constitute the test we have been expecting for our newest Federal Reserve Board Chairman - and such tests have been noted to occur during the first term for new chairmen on a historic basis.

Mr. Bernanke has made it no secret that he is prepared to allow the exchange value of the US dollar to drift lower (he has a massive balance of payments deficit to resolve). Would he and his colleagues then raise interest rates to protect the dollar, possibly precipitating a recession? Or would the FRB drop rates, sacrificing the dollar, in the hope of keeping the economy humming (this may not work in any case). Stay tuned, we may have the answer before summer is out...

April 8, 2008: This article has been one of the most visited at my website. As most readers are probably aware, the US dollar has fallen considerably further in international purchasing power since this article was written. Certainly the US dollar is now too low in terms of international purchasing parity. That is, US-based goods have become very cheap for holders of alternative currencies, particularly the Euro.

April 8, 2008: This article has been one of the most visited at my website. As most readers are probably aware, the US dollar has fallen considerably further in international purchasing power since this article was written. Certainly the US dollar is now too low in terms of international purchasing parity. That is, US-based goods have become very cheap for holders of alternative currencies, particularly the Euro.

Counterintuitively, international currency exchange markets are driven not by considerations of equivalent purchasing power (the naive observer would think they should be), but literally by supply of and demand for the currencies themselves, as commodities if you will. The core problem with the US dollar is that too many borrowed US dollars have been exported to international producers of goods and services, while demand for US-produced goods and services is in decline, maintaining the US balance of payments deficit (and with it, the US "current account") in the critically concerning $700 billion per year range.

Counterintuitively, international currency exchange markets are driven not by considerations of equivalent purchasing power (the naive observer would think they should be), but literally by supply of and demand for the currencies themselves, as commodities if you will. The core problem with the US dollar is that too many borrowed US dollars have been exported to international producers of goods and services, while demand for US-produced goods and services is in decline, maintaining the US balance of payments deficit (and with it, the US "current account") in the critically concerning $700 billion per year range.

To put that in perspective, $700 billion represents more than four times the annual revenues of the General Electric Company. So, if you will, the US is giving away to the rest of the world all the annual business of the General Electric Company four times per year, or once every calendar quarter.

I hope it is evident to you that this rate of currency devolution is simply unsustainable. That is, the US is literally bleeding dollars to the world, which so far has been "turning them around" (thereby reinfusing the US with the lifeblood of its own currency) to purchase US investments, mostly US government and corporate bonds and ownership stakes in US corporations and property.

The fear is that if the holders of US dollars lose interest in US investments (a condition which could be sparked by a US-led economic downturn), then the US will have to raise interest rates - perhaps substantially - in order to win back those foreign-held dollars, placing further pressure on the already over-stretched US economy.

An additional implication is that the US is losing ownership of its own assets at a similar $700 billion per year rate, though for the most part, so far, that has consisted primarily of US Treasury Bonds and Notes, a phenomenon which of course feeds the ongoing devaluation of the currency, but (up to this point) leaves most of the ownership of US assets in US hands.

For more recent commentary on some of these developments, particularly regarding the expanding US money supply (now at $14 trillion and recently climbing at almost 20% per year) and mounting US debts and unfunded liabilities (now approaching the $120 trillion level), please click here.

For more recent commentary on some of these developments, particularly regarding the expanding US money supply (now at $14 trillion and recently climbing at almost 20% per year) and mounting US debts and unfunded liabilities (now approaching the $120 trillion level), please click here.

Is the US dollar doomed? Click here.

Total disaster for the US dollar? Click here.

$9000 gold as the US dollar collapses? Click here.

_

Source URL: http://idontwanttobeanythingotherthanme.blogspot.com/2008/04/why-is-us-dollar-so-weak.htmlVisit i dont want tobe anything other than me for Daily Updated Hairstyles Collection

No comments:

Post a Comment